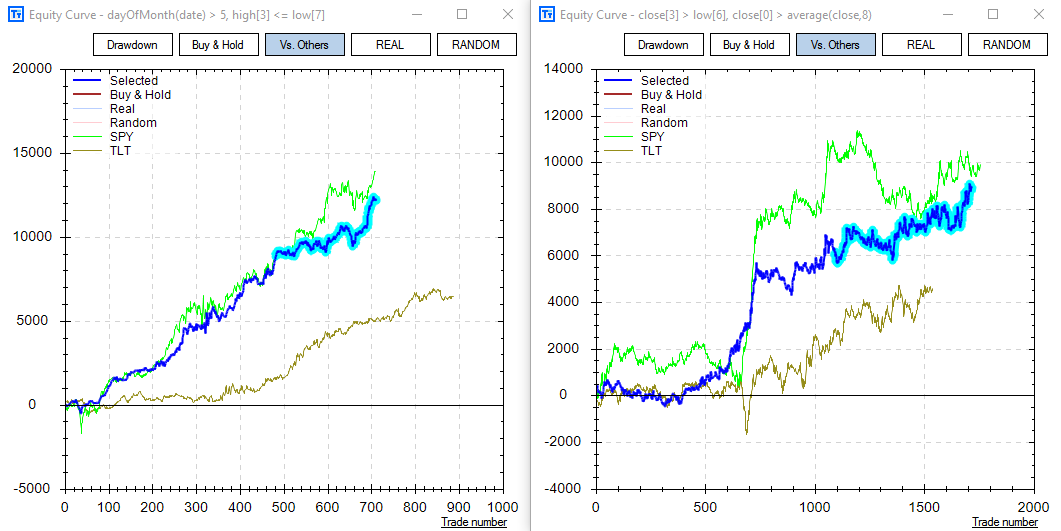

This Free Friday, Free Friday #19, is a user submission! It is a long/short strategy for $IWM – the Russell 2000 ETF. Both the long and the short strategy only have two rules each and only hold for 1 day. Below I’ve posted the long strategy on the left and the short strategy on the right. Short edges have certainly been difficult to find over the past few years in the US equity indexes on a daily time frame, but one hopes they’ll pay for the effort when/if things turn south!

Both strategies were tested from 2002 to 2017 using 35% out of sample data. All performance is based on only a simple 100 shares per trade. *1 S&P500 futures contract is equivalent to about 500 $SPY shares for reference*

There is also $SPY (green plot) and $TLT (gold plot) plotted to see how the strategies would have performed on these markets as well; the strategy maintains profitability in both cases.

The long strategy rules are simple and all trades exit at the next day’s open.

- Day number is greater than 5. Today is June 30, 2017. Today’s day number is 30.

- High[3] <= Low[7]

The short strategy rules are simple as well and all trades exit at the next day’s open.

- Close[3] > Low[6]

- Close[0] > 8 Period Simple Moving Average

Below there is a photo of the long/short equity performance for this simple portfolio.

I also want to add an update to some of the Free Friday strategies. Things were pretty quiet for most of the futures strategies other than the equity index strategies this month.

Strategies #5, #6, #16 were the only futures strategies that traded so I wanted to show their June performance below.

Nasdaq #5: +$1,640.00

Russell Futures #6: +680.00

S&P500 Futures #16: +862.50

Russell Futures #6: +680.00

S&P500 Futures #16: +862.50

Again, all are just trading 1 contract for demonstration purposes and were posted publicly months ago. You can see the strategies on twitter here: @dburgh

Thanks as always and have a Happy Fourth of July,

Author

David Bergstrom – the guy behind Build Alpha. I have spent a decade-plus in the professional trading world working as a market maker and quantitative strategy developer at a high frequency trading firm with a Chicago Mercantile Exchange (CME) seat, consulting for Hedge Funds, Commodity Trading Advisors (CTAs), Family Offices and Registered Investment Advisors (RIAs). I am a self-taught programmer utilizing C++, C# and python with a statistics background specializing in data science, machine learning and trading strategy development. I have been featured on Chatwithtraders.com, Bettersystemtrader.com, Desiretotrade.com, Quantocracy, Traderlife.com, Seeitmarket.com, Benzinga, TradeStation, NinjaTrader and more. Most of my experience has led me to a series of repeatable processes to find, create, test and implement algorithmic trading ideas in a robust manner. Build Alpha is the culmination of this process from start to finish. Please reach out to me directly at any time.