For this week I want to discuss personal comfort regarding sample size or number of trades. I often get asked to generate strategies that are more “swing-trade” oriented and hold for days to weeks.

I have no problem with these types of strategies and Build Alpha can certainly build them. This Friday’s strategy is exactly that, but at the end I explain my thoughts regarding this style of trading.

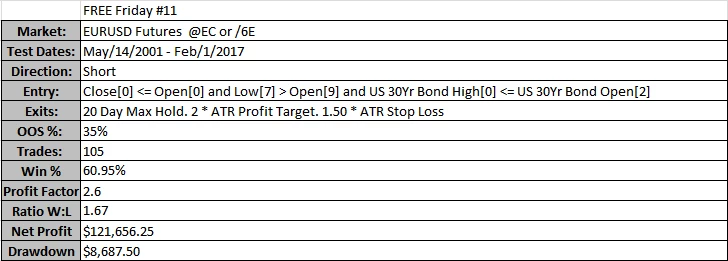

This strategy shorts the EURUSD futures whenever these 3 conditions are true:

- Today’s close is below today’s open

- Low[7] > Open[9]

- US 30Yr Bond’s High[0] <= US 30Yr Bond’s Open[2]

The exit conditions for this strategy are as follows:

- Maximum hold of 20 days

- 2.00 * 20 Period ATR Profit Target (Calculated at Entry)

- 1.50 * 20 Period ATR Stop Loss (Calculated at Entry)

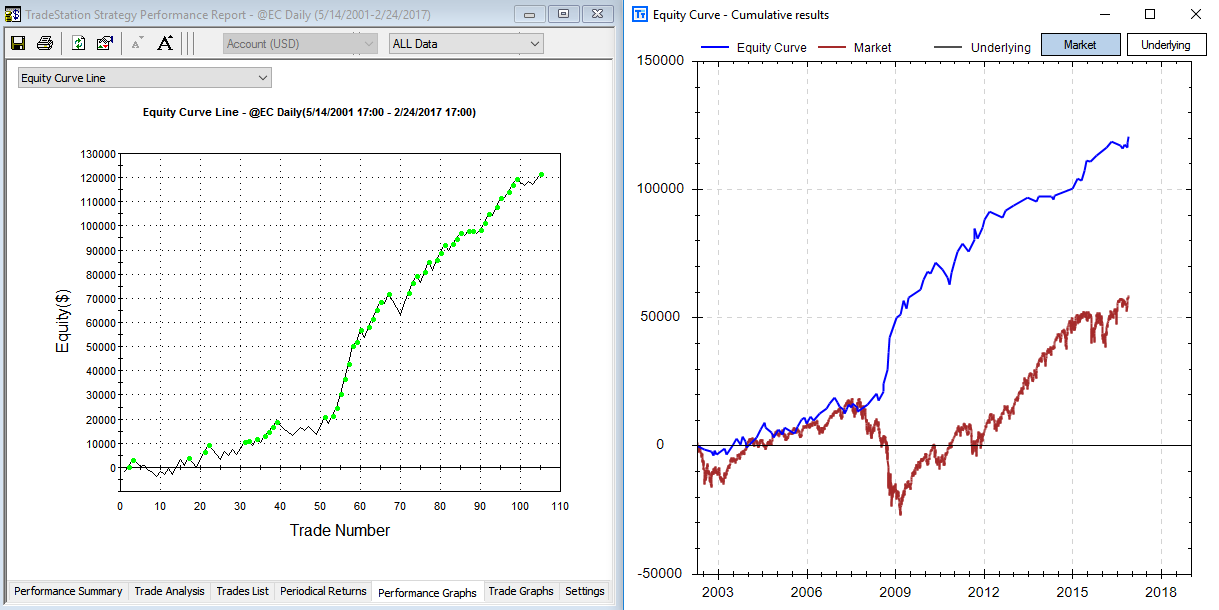

Below I’ve attached a chart of the equity curve in TradeStation (left – by trade number) and the equity curve vs. S&P500 on the right generated by Build Alpha (by date).

As you can see these type of exits drastically reduce the number of trades (compared to say a 1 day maximum hold). Without getting technical, the more trades the lower the chances the strategy may be a “fluke”.

This strategy’s out of sample period began in 2012 which means that this strategy has had its last 20+ trades on “unseen” data and did quite well.

Some may say that is fine and they’re ready to proceed with this strategy, but others may say that this is not enough trades. This essentially comes down to personal preference.

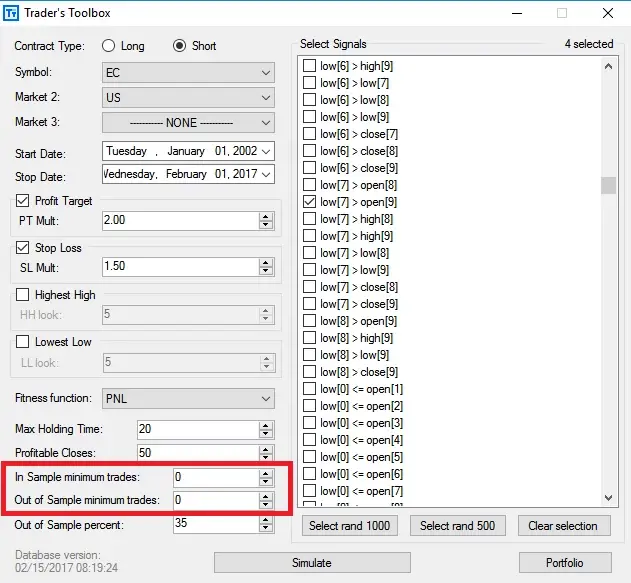

The important note I’d like to make is… Build Alpha allows you to discard strategies that the software generates that do not have a certain number of trades.

For example, your personal preference might require at least 500 out of sample trades. If so, you would simply enter that number into Build Alpha and the software would then discard any strategies that do not trade frequently enough during the strategy generation process.

Happy Friday,

Old Posts:

Author

David Bergstrom – the guy behind Build Alpha. I have spent a decade-plus in the professional trading world working as a market maker and quantitative strategy developer at a high frequency trading firm with a Chicago Mercantile Exchange (CME) seat, consulting for Hedge Funds, Commodity Trading Advisors (CTAs), Family Offices and Registered Investment Advisors (RIAs). I am a self-taught programmer utilizing C++, C# and python with a statistics background specializing in data science, machine learning and trading strategy development. I have been featured on Chatwithtraders.com, Bettersystemtrader.com, Desiretotrade.com, Quantocracy, Traderlife.com, Seeitmarket.com, Benzinga, TradeStation, NinjaTrader and more. Most of my experience has led me to a series of repeatable processes to find, create, test and implement algorithmic trading ideas in a robust manner. Build Alpha is the culmination of this process from start to finish. Please reach out to me directly at any time.