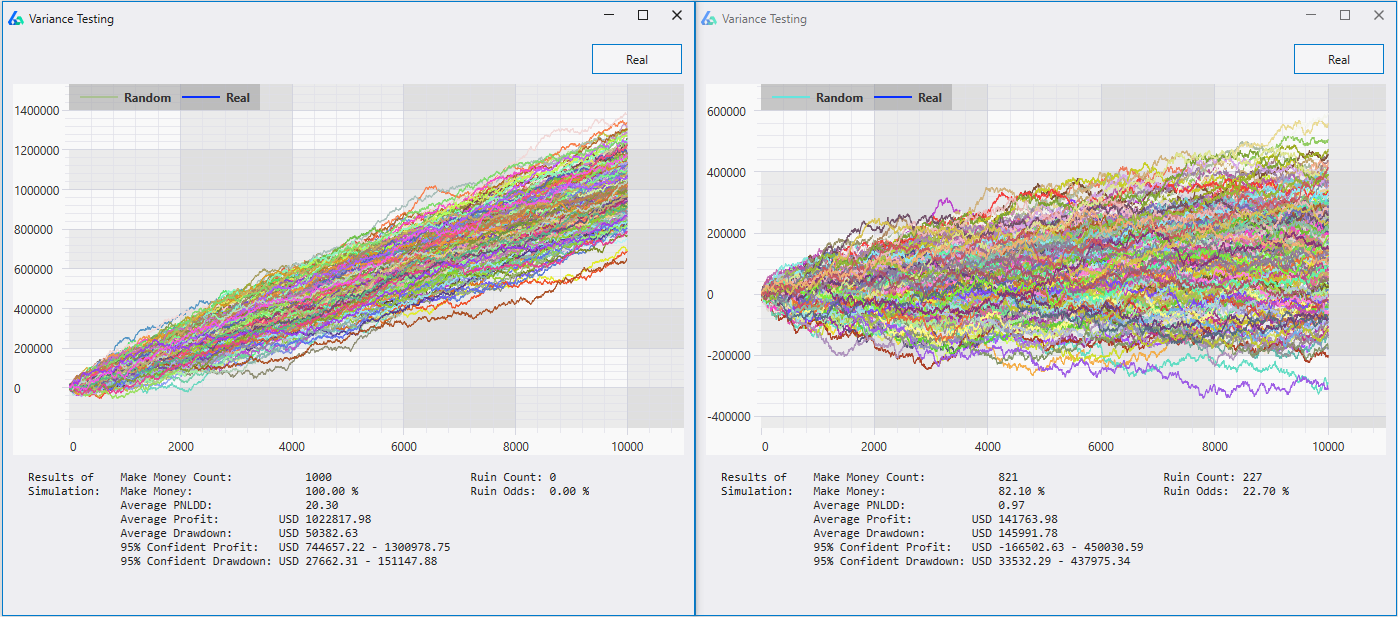

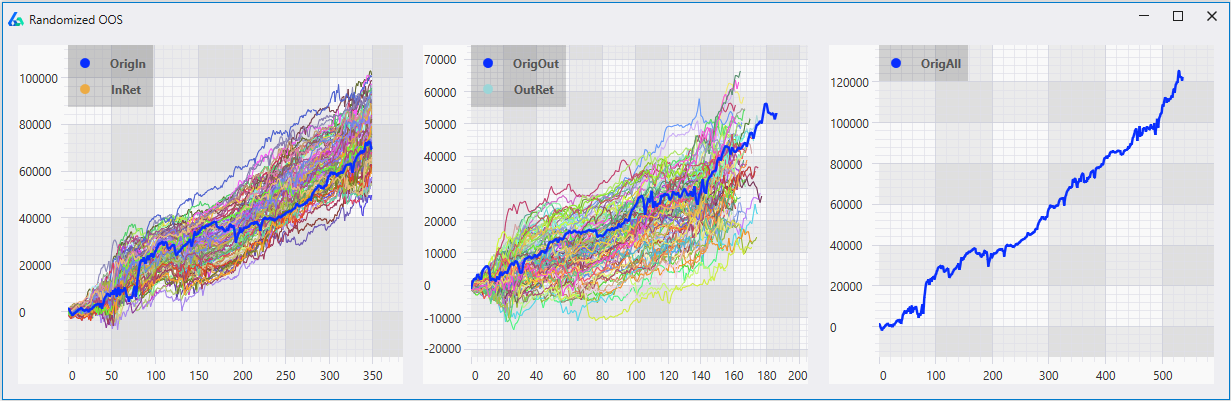

Example of Variance Testing

For example, a trader or money manager can vary his win rate and see how likely a certain strategy is to make $X over the next 100 trades or how likely said strategy is to lose $X over the next 100 trades given a certain fluctuation in the winning percentage.

Setting Realistic Trading Expectations

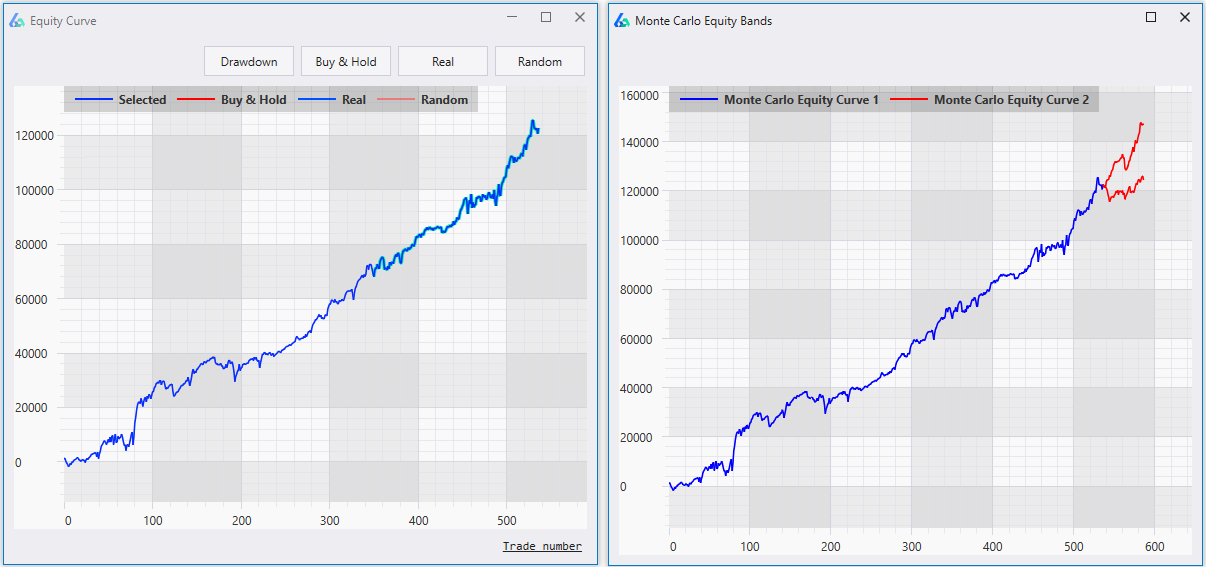

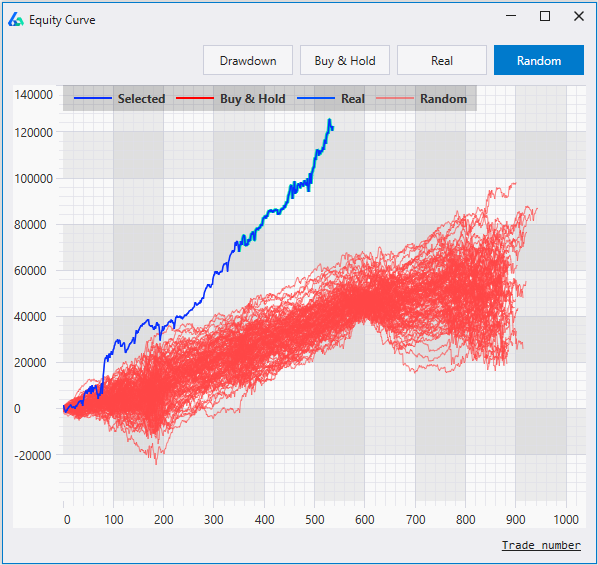

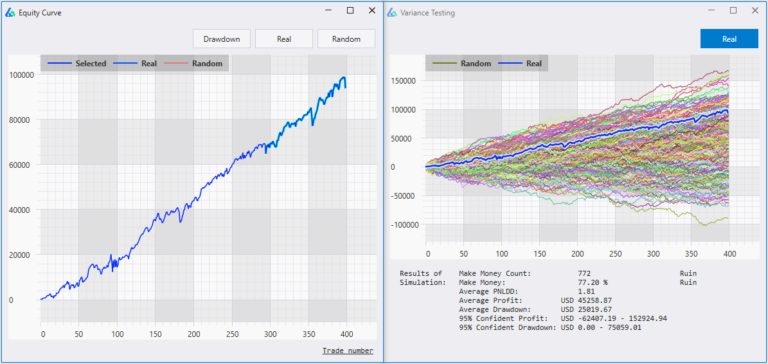

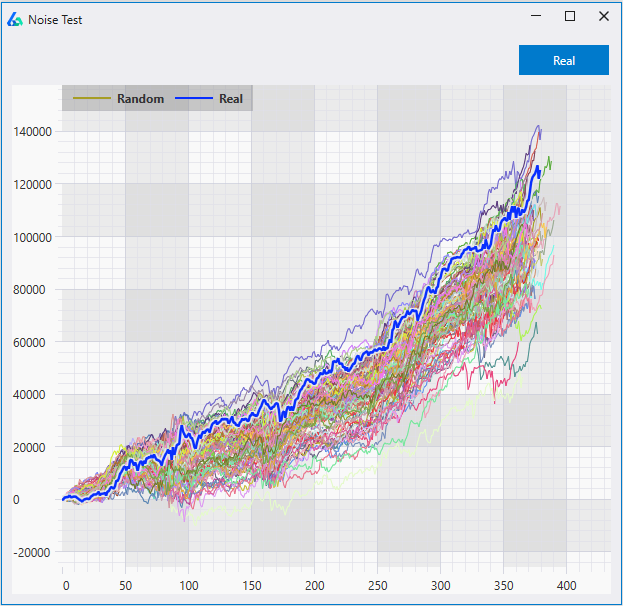

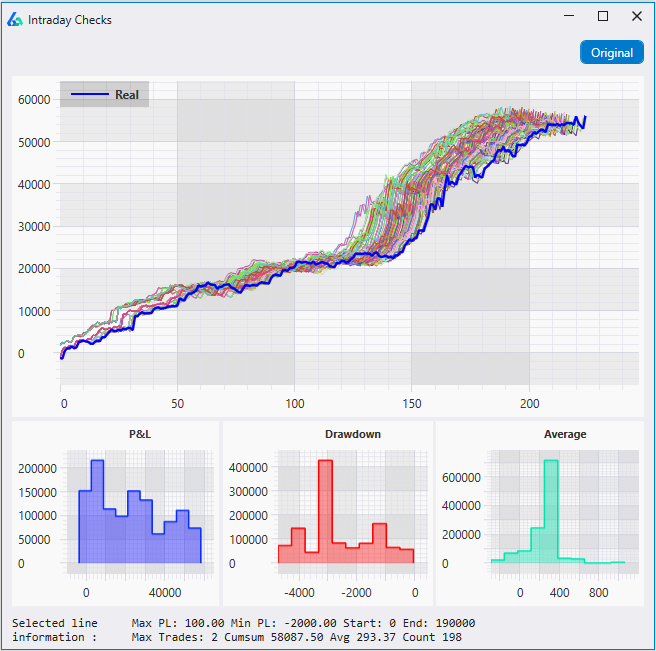

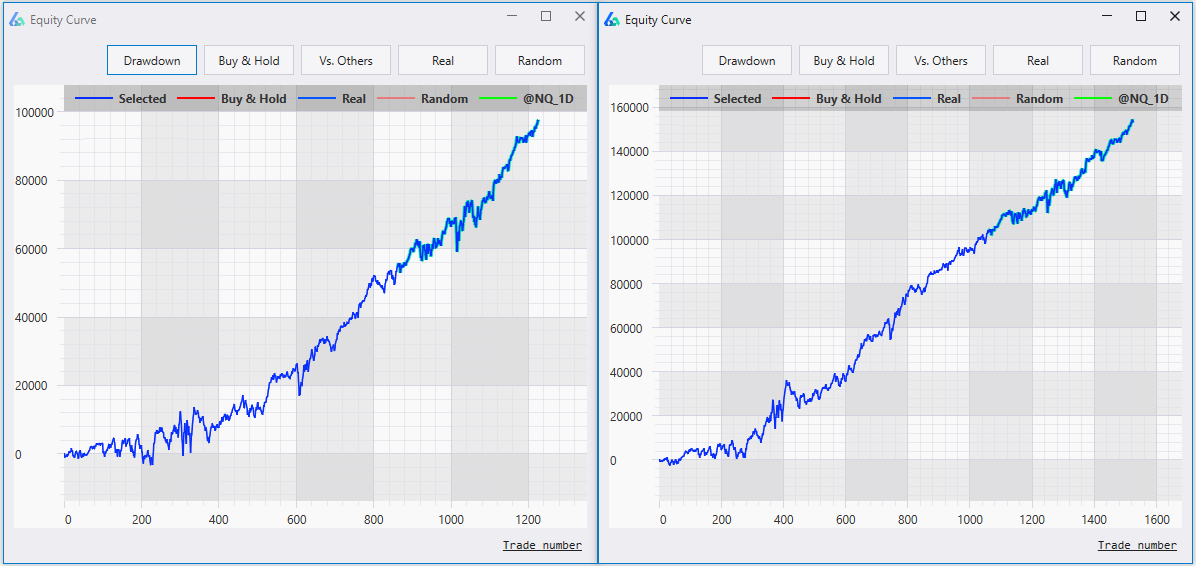

Similarly, one main goal is to prevent clients from saying “all my systems fail when they go live”. The problem may very well be the trader or money manager had unrealistic expectations heading into live trading. For example, did the strategy display a distribution like the one on the left picture above or the distribution like the picture on the right?

If you do not know then you are not prepared and likely will say, “all my systems fail when they go live”. This type of stress testing can help determine if a strategy had an unrealistic backtest or is part of a stable distribution poised to perform near desired expectations moving forward.

Variance Testing Details

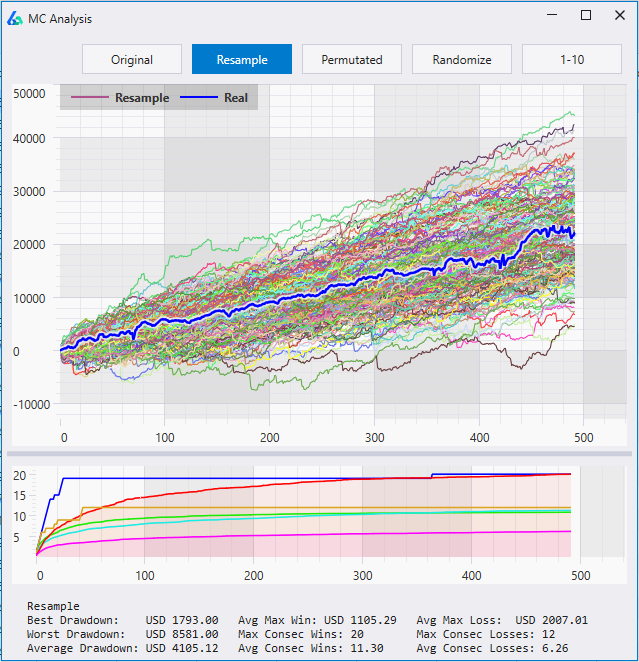

Beneath the graph, Variance Testing also displays

- likelihood a strategy will be profitable over N trades

- likelihood it will hit a certain drawdown over N trades

- average profit and drawdown over X number of simulations

- 95% confidence interval for both profit and drawdown.

All of these data points can help create better expectations moving forward while helping traders and money managers avoid fatal (and avoidable) mistakes. Build Alpha users can adjust the number of trades looking forward, the number of simulations, the drawdown amount, and the win rate’s variance to build their own custom stress test on every strategy AND portfolio constructed.